Store brand unit sales in the U.S., on the heels of a strong finish in Q4 of 2025, carried that momentum into the new year with a solid 2.3% gain for the period ending January 25, according to PLMA’s research partner, Circana. Store brand dollar sales for the month were also positive, up by 2.3%.

True to its form of the past several years, store brands in 2025 continued to serve as a bright beacon in the overall U.S. retailing landscape—satisfying consumer needs with high quality, value-driven product solutions; achieving, and in many cases exceeding, retailer goals for enhanced marketplace differentiation and performance; and, along the way, establishing new records for annual revenue as well as dollar and unit sales and shares.

According to PLMA’s 2026 Private Label Report, “A Bright Beacon In U.S. Retail Landscape,” store brand dollar sales in the year increased nearly three times the rate of national brands as the products surged ahead by 3.3% compared to a gain of only 1.2% for their national brand counterparts. Looking at unit sales, the head-to-head difference was comparable. Store brands advanced by 0.6% while national brands declined by -0.6%.

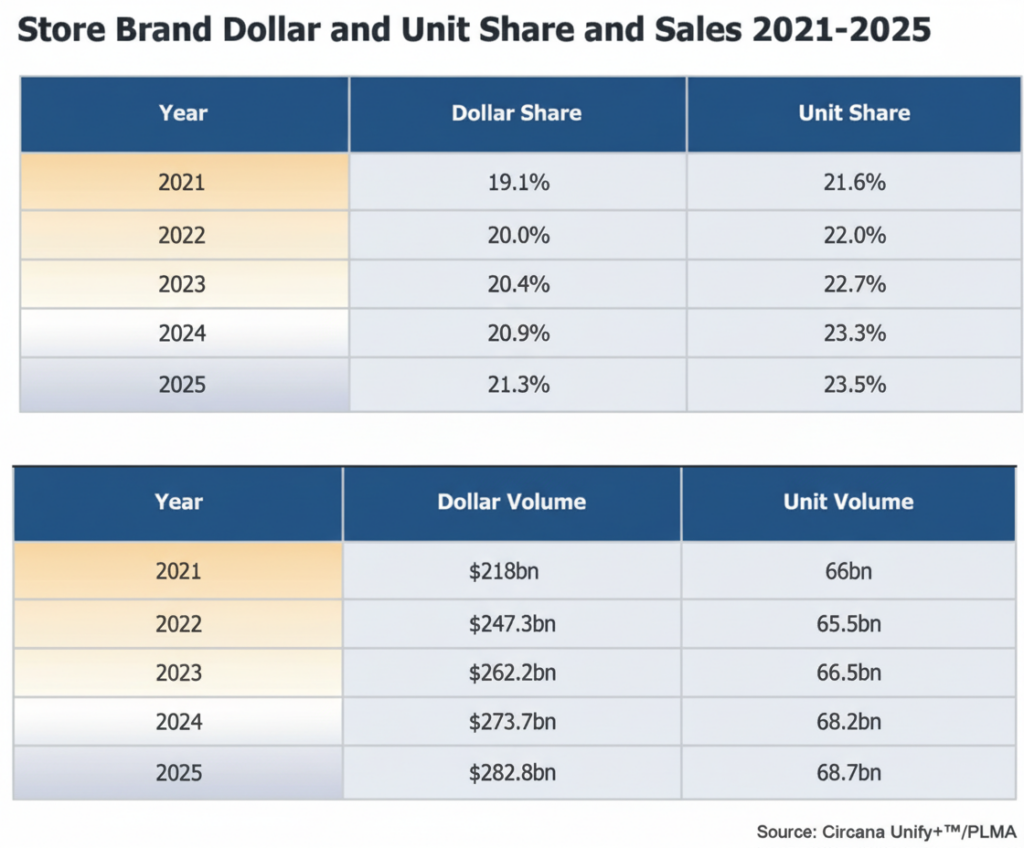

In all outlets, total store brand revenue for 2025 surpassed a quarter trillion dollars for the second year in a row, coming in at $282.8 billion, an increase of slightly more than $9 billion over 2024 and establishing an all-time high in annual volume. Store brand unit volume was up by 434.3 million to 68.7 billion, also setting a new record. National brands lost 1.43 billion units.

Retailers are launching lines to defend and expand their private label reach, according to Circana. Key new initiatives include Kroger’s Smart Way and Mercado, Walmart’s bettergoods, Target’s Deal Worthy and Figmint, Amazon’s Saver and CVS’ Well Market.

“Retailers are doubling down on private labels as a strategic asset for differentiation, brand building and creating emotional bonds with shoppers. Through innovation, pricing and promotion excellence at their grassroots,” says Sally Lyons Wyatt, Circana’s Global EVP & Chief Advisor, Consumer Goods & Foodservice Insights.

“Private brands’ growth reflects a fundamental shift in consumer priorities. Retailer-owned brands are increasingly competing —and winning—on value, quality, efficacy, and sustainability,”

“From the perspective of sales and shares, 2025 was U.S. store brands’ most successful year ever,” declared PLMA’s President, Peggy Davies. “It was a year of achievement across the board, including the growing recognition of the strategic importance of store brands by the trade and consumer media, the investor and consultant community and, most importantly, by the C-suite at America’s retailers. Not coincidentally, it was a banner year for PLMA, as well, highlighted by the bestattended Chicago Trade Show ever and the well-received inauguration of Store Brands Month.”

Some experts predict the gap between the market share penetration of private label grocery products in the U.S. vs Europe will narrow. They may be on to something. Over the past two years, when measured alongside Europe’s top 17 private label markets, American store brands ranked 6th in dollar share increase, +0.8 points, and 9th in unit share gain, +0.9 points.

“Private brands’ growth reflects a fundamental shift in consumer priorities. Retailer-owned brands are increasingly competing —and winning—on value, quality, efficacy, and sustainability,” continued Davies.

In fact, according to Alvarez & Marsal Global, “store brands’ boom is financially driven by highearning, over $100,000 households, 82% of whom are increasing their private label purchases, outpacing lower-income groups…private label growth is a permanent market shift, not merely a temporary response to inflation.”

“Consumer trust and trial show continued acceptance and willingness to explore new private brand products, even in traditionally brand-dominated spaces. All generations are more open to trying new private label products, though younger consumers are most adventurous,” claimed Circana in its 2025 report, From Growth to Transformation: The U.S. CPG Private Label Story.

“Private labels of the future will see broad investment not just from major retailers, but also from regional and mid-sized players. Economic uncertainty will continue to elevate private brands. Quality and innovation will continue to be the focus, while emerging trends in sustainability and localization gain emphasis.”

Once consumers switch to private label, brands face an uphill battle to win them back. By offering highquality products at lower price points, chains reset what shoppers expect for the money. Private labels are sticky, and the longer consumers stay switched, the harder it becomes for brands to reclaim lost ground.

“The ‘value luxury’ trend is the strategic pivot by grocers to elevate store brand quality and design, making them aspirational purchases preferred by high-income consumers seeking efficacy and value. They’re also setting aggressive goals, such as Albertsons aiming for 30% private label share. Aldi’s decision to unify branding under its name emphasizes confidence in its private label quality to carry the store’s reputation. These moves confirm a long-term industry shift where private label is a central pillar of operations,” said research firm Insight Trends World.

PLMA’s 2026 Private Label Report is available online at plma.com. Retailers and PLMA members enjoy 24-7 access to real time store brand and national brand sales data through PLMA’s partnership with Circana’s Unify+.